BOU FINALLY WAKES UP! New Cash Withdrawal Caps Expose Years of Lax Oversight After Parliament Corruption Probe Closes in on Anita Among’s Inner Circle Money Trail

For years, Uganda’s banking halls have witnessed scenes that should have set off alarm bells at the highest levels of financial regulation. Bags of cash moving in and out. Millions and sometimes billions of shillings withdrawn over the counter. Multiple accounts being operated by politically connected individuals. Transactions so large and so frequent that ordinary Ugandans could only dream about them.

Yet somehow, the system appeared comfortable.

Now, in what many observers are describing as a case of “too little, too late,” the Bank of Uganda (BoU) has unveiled sweeping new restrictions on cash withdrawals and interbank cheque transactions, a move that has reignited questions about whether the country’s financial watchdog slept on the job as suspicious transactions flourished under its nose.

The development comes at a particularly explosive moment.

Investigators probing alleged corruption, money laundering and illicit enrichment at Parliament are reportedly tracing vast sums of money through multiple bank accounts linked to staff, associates and individuals close to former Speaker Anita Among.

The timing has left many Ugandans asking one uncomfortable question: Why is the central bank only acting now?

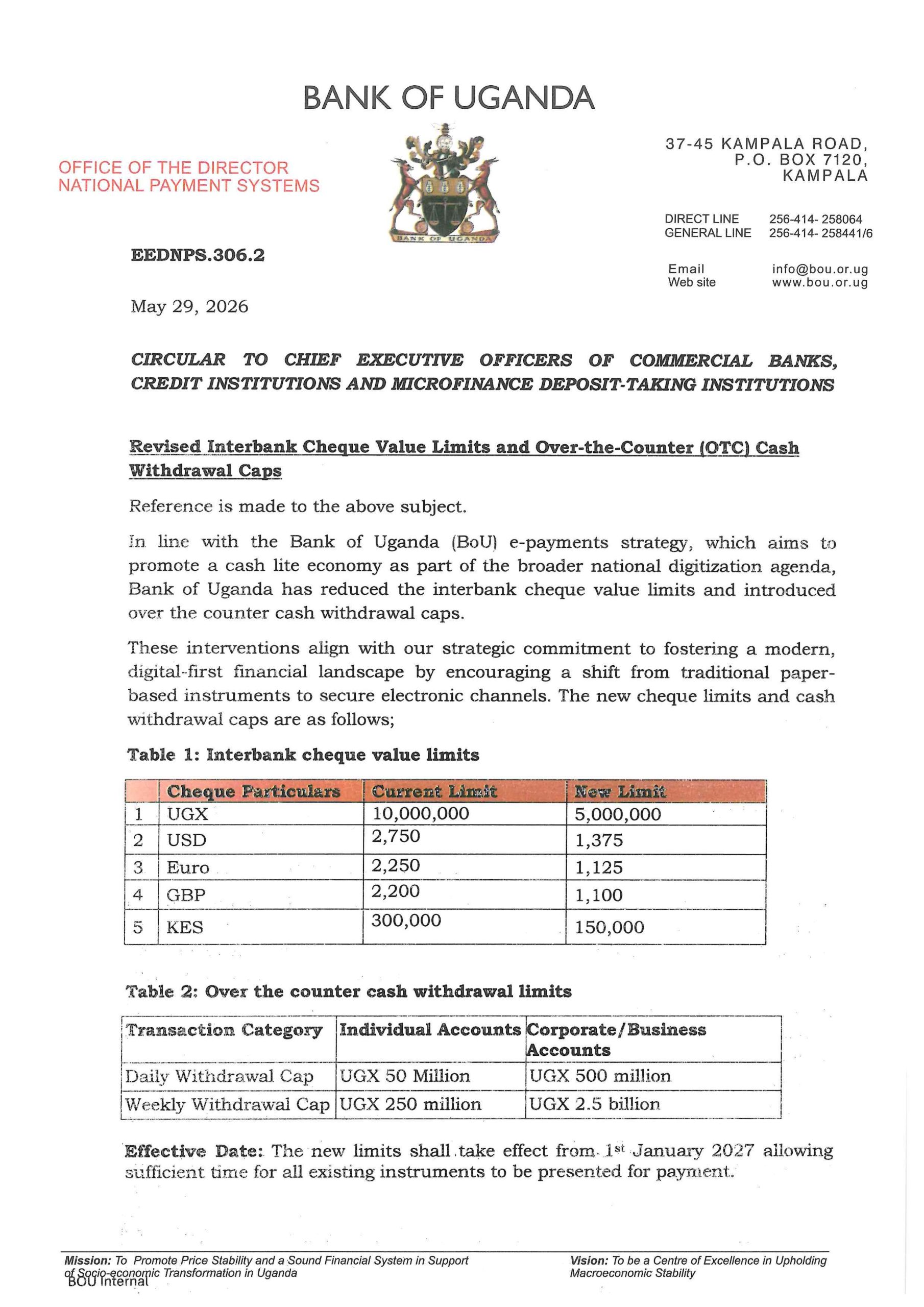

Under the new directive, individual account holders will be restricted to over-the-counter withdrawals of Shs50 million per day and Shs250 million per week, while companies and businesses will face daily limits of Shs500 million and weekly caps of Shs2.5 billion.

The directive also slashes interbank cheque limits across several currencies and seeks to force greater use of electronic payment systems.

The directive, issued by Bank of Uganda Executive Director for National Payment Systems, Dr. Tumubweinee Twinemanzi requires all chief executives of commercial banks, credit institutions and microfinance deposit-taking institutions across the country to take note.

Bank of Uganda says the new restrictions are part of its strategy to promote a cash-lite economy and support Uganda’s broader digital transformation agenda. The central bank says the measures are intended to encourage migration from paper-based and cash transactions to more secure electronic payment platforms.

The new limits will only take effect on January 1, 2027, giving financial institutions and customers time to adjust and allowing existing instruments to be cleared from the system.

The directive was issued under Bank of Uganda’s mission of promoting price stability and a sound financial system in support of Uganda’s economic transformation and its vision of becoming a centre of excellence in upholding macroeconomic stability.

However, beyond the official explanation lies a much bigger debate.

Coming at a time when investigators are digging deep into alleged cash movement networks linked to Anita Among and several public officials, many observers are finding it difficult to separate the directive from the country’s biggest ongoing corruption probe.

For years, the Auditor General has repeatedly highlighted weaknesses in financial controls, accountability systems, cash management practices and oversight mechanisms across government institutions.

Again and again, audit reports raised concerns about poor supervision, weak internal controls and systems that allowed public funds to be irregularly spent or insufficiently accounted for.

Yet despite those warnings, huge volumes of cash continued moving through the banking sector under BoU watch.

Now those same concerns appear to be resurfacing in the Parliament corruption investigation.

The probe, which began on May 16, 2026 and initially focused on former Speaker Anita Among, has rapidly expanded beyond Parliament’s top leadership.

Teams comprising detectives from CID, Crime Intelligence, forensic services and security agencies have spent weeks examining properties, bank records, transaction histories and financial networks believed to be linked to the investigation.

Searches at residences in Nakasero, Kigo, Ntinda and Bukedea have already resulted in the seizure of several luxury vehicles, including the Rolls-Royce that reportedly triggered heightened scrutiny of the former Speaker’s wealth.

But investigators are increasingly interested in something far more significant than luxury cars.

Money trails.

According to sources close to the investigation, forensic teams are scrutinising numerous bank accounts allegedly linked to parliamentary staff and individuals believed to have handled cash transactions connected to powerful figures within Parliament.

The accounts reportedly span departments including Transport, Finance, Protocol, Public Affairs and Communications.

Sources claim investigators are examining allegations that enormous sums of money passed through multiple accounts before being withdrawn in stages.

In some instances, more than Shs2 billion is alleged to have moved through the banking system within a single day.

Investigators are also reportedly examining claims that funds were channelled through accounts belonging to drivers, cleaners and security personnel attached to influential offices.

Some account holders allegedly benefited financially after allowing their accounts to be used for transactions.

If proven, the allegations would expose a sophisticated cash movement network operating within a financial system that is supposed to be protected by strict anti-money laundering controls.

And that is precisely where the spotlight is now shifting.

Uganda already has laws requiring banks and financial institutions to identify suspicious transactions, profile high-risk customers, monitor unusual activity and report suspicious dealings to authorities.

The question now confronting regulators is whether those safeguards were being properly enforced.

If billions of shillings were allegedly moving through multiple accounts linked to politically exposed individuals, how did those transactions avoid attracting stronger scrutiny?

Were suspicious transaction reports filed?

Did regulators act on them?

Were red flags ignored?

Or were the systems simply ineffective?

What makes the latest directive particularly revealing is that Bank of Uganda itself appears to acknowledge many of the vulnerabilities critics have been raising for years.

The central bank now requires all supervised financial institutions to maintain robust and continuously updated risk-based customer profiles. These profiles must be used when determining and reviewing withdrawal limits for both individual and corporate customers.

Banks will now be expected to demonstrate that cash withdrawal thresholds are informed by ongoing due diligence, customer risk assessments and regular monitoring.

That requirement immediately raises uncomfortable questions.

If customer profiling and risk assessments are now considered critical safeguards, were they being adequately enforced before?

And if they were, how did alleged billion-shilling transactions linked to politically exposed individuals at parliament continue moving through the system without triggering stronger interventions?

The directive also acknowledges that some sectors, particularly agriculture and artisanal mining, remain heavily dependent on cash transactions. As a result, Bank of Uganda has created an exception mechanism allowing financial institutions to apply for waivers on specific transactions or sectors.

However, such exemptions will only be granted after comprehensive risk assessments and detailed customer due diligence, placing even greater emphasis on controls that critics argue should have been aggressively enforced long ago.

The circular further requires banks to actively steer customers toward digital payment channels including Real-Time Gross Settlement (RTGS), mobile banking, internet banking and other electronic platforms.

Financial institutions must now demonstrate that they are proactively advising customers to use digital alternatives and making those services readily accessible.

Bank of Uganda says it will spend the six-month transition period working with stakeholders to conduct nationwide public awareness campaigns aimed at preparing customers and institutions for the new regime.

The central bank has also reserved the right to periodically review and adjust the withdrawal limits in consultation with the financial sector.

Ironically, government and financial regulators have spent years promoting digitisation as a key weapon against corruption because electronic transactions create clearer audit trails and reduce opportunities for concealment.

Yet despite that policy direction, enormous sums of money allegedly continued circulating through cash-heavy channels that are harder to monitor and easier to hide.

That contradiction is why the new measures are attracting both praise and scepticism.

Supporters argue that tighter controls are long overdue and could significantly reduce opportunities for abuse.

Critics argue that regulators are only reacting after investigators uncovered troubling patterns that should have been detected years earlier.

The pressure on institutions is only likely to intensify as the Parliament probe widens.

Investigators are reportedly examining transactions involving numerous parliamentary departments, while several officials have either recorded statements or are expected to be summoned for questioning.

There are also reports that former parliamentary commissioners could be required to explain allegations surrounding the sharing of at least Shs1 billion.

As investigators continue following the money trail, attention is increasingly turning toward the banking sector and the regulators responsible for safeguarding it.

For many Ugandans, the issue is no longer simply about withdrawal limits.

It is about accountability.

It is about whether institutions entrusted with protecting the country’s financial system acted with sufficient vigilance.

It is about whether warning signs highlighted repeatedly by the Auditor General were taken seriously.

It is about whether billions of shillings moved through the banking system because controls were weak, oversight was inadequate or enforcement was simply absent.

And it is about whether one of the country’s biggest corruption investigations has finally forced regulators to confront weaknesses that should have been addressed years ago.

GOT A HOT STORY? EMAIL: redpeppertips@gmail.

SOURCE PROTECTION/CONFIDENTIALITY IS OUR NO.1 PRIORITY.